Note: This resource is primarily intended for individuals navigating insurance within the U.S. healthcare system. This content does not constitute professional medical advice. The information is included for informational purposes only and cannot guarantee coverage for any medical services.

Health Insurance Basics

Health insurance plans are designed to cover some or all of the costs of medical care for an individual or family. Not all plans are the same. In fact, they can differ quite a bit! Understanding some basic health insurance terminology and the answers to some common questions can help you make informed decisions about your health insurance.

In addition to reading through the information below, you can also visit the “Resources” section of this guide for links to more information on health insurance.

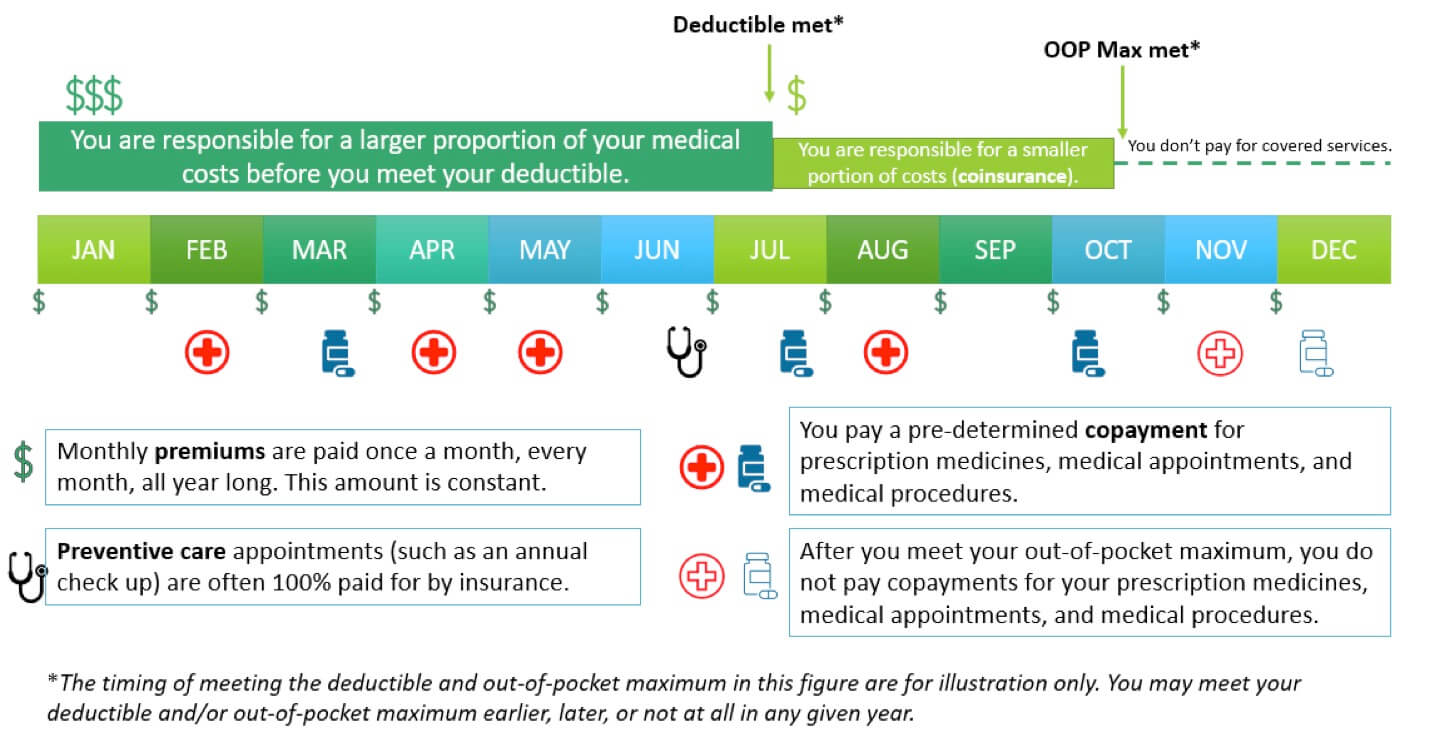

Premium: A fixed amount you pay to the insurance company each month to be covered by their plan. Premiums do not count toward deductibles or out-of-pocket maximums. If you have health insurance through your employer, they may pay part or all of your premiums for you.

Copayment (“Copay”): A fixed amount you are expected to pay for a service (for example, a doctor’s appointment or a prescription refill). You may still have a copay for these services even after you’ve reached your deductible. Your copay usually does not count toward your deductible, but it does count toward your out-of-pocket maximum.

Coinsurance: A percentage you are expected to pay for a covered service or a procedure after you meet your deductible. For example, you may be expected to pay 20% after you reach your deductible. Before you meet your deductible, you pay 100% of the cost of these services. Your insurance plan should outline which services are subject to copayments and which services are subject to coinsurance. Coinsurance applies until you’ve reached your out-of-pocket maximum.

Deductible: The amount of money you have to pay for certain covered services in a year before your health insurer starts sharing the cost. Some services may be fully covered before you meet your deductible. Copayments and premiums do not count toward your deductible. You will still share some of the cost for your medical services after you’ve reached your deductible until you have reached your out-of-pocket maximum.

Out-of-pocket maximum (OOP): The maximum amount of money you have to pay in a year before your health insurer will pay 100% of the bills for remaining covered services that year. The OOP maximum is often different for In-Network and Out-of-Network services. Your deductible, coinsurance, and copayments all count toward your out-of-pocket maximums. This only applies to covered benefits. Payment for non-covered services do not count toward your OOP maximum. Premiums do not count towards your OOP maximum.

Figure: Visual representation of health insurance costs.

Covered service: A service that is seen as medically necessary and within the bounds of your insurance agreement. Insurance plans differ in what services they cover. Covered services are not free (except in certain circumstances like preventive care); you must pay any copay or coinsurance as outlined in your insurance agreement.

Non-covered service: A service that is not medically necessary or not within the bounds of your insurance agreement. You will be responsible for the full bill for any non-covered service you receive, and it will not count toward your deductible or out-of-pocket maximum.

Preventive care: Services such as an annual well check-up which are recommended to keep people healthy. Many preventive care services are covered 100% by insurance plans and don’t require you to pay copayments or coinsurance. Some types of common cancer screenings (such as colonoscopy or mammogram) may also be considered preventive care. Preventive screenings specific to a particular cancer syndrome, such as LFS, may not be covered to the same extent as other preventive cancer screenings recommended for the general population.

In-network: Providers and healthcare systems that have special agreements and often negotiated pricing with your insurance company. Even before you meet your deductible or out-of-pocket maximum, you cannot be billed more for an in-network covered service than what the insurance company has negotiated with the provider ahead of time. In-network providers are also known as “preferred providers” or “participating providers,” though there may be slight nuances to these terms depending on your plan.

TIP: It can often be cheaper to use in-network providers and services. Before scheduling an appointment or procedure, you can contact your insurance company to check if the provider or facility is in-network. If not, you may be able to work with your doctor and insurance company to find in-network options. Even if a facility, such as a hospital, is in-network, it does not mean that all providers at that facility are also in-network.

Out-of-network: Providers and healthcare systems that do not have special agreements or negotiated pricing with your insurance company. Expect your copayments and coinsurance to be higher for services performed out-of-network.

Preferred provider organization (PPO): PPO plans do not require you to establish care with a primary care physician (PCP) or to obtain referrals from your PCP before seeing a specialist. PPO plans typically allow you to receive out-of-network care, though they will generally expect you to pay more in those instances. PPO plans provide quite a bit of flexibility, but they also usually have higher monthly premiums and out-of-pocket costs.

Point of Service (POS): POS plans have some features of both HMO and PPO plans. They require you to establish care with a primary care physician (PCP) and may require referrals from your PCP before you can see other specialists. However, POS plans do allow some flexibility for patients to see out-of-network providers, though this will cost more than in-network.

Exclusive provider organization (EPO): An EPO plan also has overlapping features with HMO and PPO plans. They may or may not require you to establish care with a primary care physician (PCP); however, they do not require a referral in order to see other medical specialists. They typically do not cover out-of-network care. An EPO plan is cheaper than a PPO plan but may have a higher deductible.

High deductible health plan (HDHP): As the name implies, a HDHP is a health plan with a high deductible. This is currently (as of 2022) defined as a plan with a deductible of $1400 or more for an individual ($2800 or more for a family). An HDHP is most appropriate for generally healthy individuals since monthly premiums tend to be low, but costs can be high when someone gets sick, since the deductible is high. These types of plans qualify for health savings accounts (described under “Billing” below) which can help a person be prepared in the event of a high expense year.

Explanation of Benefits (EOB): This is not a bill. Your EOB is mailed to you from your insurance company and outlines the details of a service you received, including the date of service, description of the service, who performed the service, what was charged for the service, what was the amount allowed to be paid for the service (the agreed upon rate between provider and insurance company), what insurance paid, and what you owe the provider (deductible, copayment, co-insurance). Often the charged amount is higher than the allowed amount. For in-network services, this charge is not passed on to the patient. However, it is possible for an out-of-network provider to “balance bill” the patient if a service is not fully covered by the insurance.

You can use your EOB to make sure the bill you receive from your healthcare system or provider is correct. If your EOB and bill do not match, you should figure out what is causing the discrepancy by contacting your insurance company and/or the provider’s billing office before you pay your bill. Your insurance company will never bill you for medical services; bills come from the healthcare system or provider that performed the service.

Sometimes you may receive communication from your insurance company that a particular service is not covered or that they are working out a request for coverage with your provider. These types of communications are different from an EOB. If you receive a communication from your insurance company regarding your coverage and do not understand the details in the communication, it is important to contact them to have your questions answered.

Tip: You can call your insurance company and/or the billing department (usually their contact info is right on the bill or EOB) if you have any questions about your bill or EOB. They can be very helpful to assist you in understanding your charges and coverage and answer any questions you may have.

Health savings account (HSA): An HSA is a special savings account that allows you to save pre-tax money to pay for medical expenses. Only people with high deductible health plans (HDHP) can open an HSA. Money deposited in an HSA is completely tax-free and can be used to pay for approved medical expenses. Money not used in a given year will roll over to the next year, but there are limits to how much a person can deposit into the account. You may need to submit your medical receipts to your HSA administrator to have your bill paid or reimbursed with your HSA funds. An HSA is “portable” meaning that it stays with you if you change jobs.

Flexible spending account (FSA): A flexible spending account (also called flexible spending arrangement) is similar to an HSA because it allows you to save a certain amount of pre-tax money to cover medical expenses. However, there are limits to how much money, if any, can roll over if you don’t use it all in any given year. An FSA is only available through an employer, so if you have an FSA through your work, you may lose the money in your account if you change jobs. You do not have to have a high deductible health plan (HDHP) to qualify for an FSA.

Resources

FAQs

Insurance Appeal Letters For Care Providers

Additional Resources

Webinar Dollar For: Navigating Hospital Financial Assistance

Download the Insurance Basics for Individuals with Li-Fraumeni Syndrome (LFS) PDF

Cancer Today: Cancer’s Financial Impact on Young Adults (winter 2025/2026). Includes Financial Resources (click red box)